So Friday (23rd September) turned into a big day …

Liz Truss and Kwasi Kwarteng, the “current” Chancellor of The Exchequer (I’m saying current because there’s been so many changes recently it’s getting harder to keep up) promised to pull a rabbit out of the hat. I think it’s fair to say nobody predicted what they did.

Here’s a quick low down.

Reduction In Income Tax….

The additional rate of tax, payable at 45% on income over £150,000 has been removed completely. The highest rate of tax you will pay now is 40%, on anything over £50,270. Admittedly, I don’t think this will have much of an impact on many of our clients.

If you were thinking, “Good for the rich,” then they also announced that the basic rate of income tax will drop from 20% down to 19% in April 2023. A 1% drop in income tax is a big headline, but in reality, it won’t be that different. It will likely only be a difference of up to £500 more in your pocket next year.

… And the knock on affect to pensions?

We were all getting too comfortable with our mental maths anyway. Whether that was calculating 20% of income or grossing up your personal pension contributions. Now, we need to learn how to gross up your contribution by 19%.

For example, if you’re paying £800pm personally into your pension, the pension reclaimed the income tax and this grossed up to £1,000pm. Now, to get £1,000pm into your pension, you’ll need to pay £810pm. If you don’t change, you’ll only get £987.65 into your pension.

This leads to an interesting question for anyone with a Lifetime ISA. It benefits from a flat bonus of 20%, compared to your pension getting relief at 19%.

National Insurance Contributions

Removing the 1.25% levy added on to National Insurance Contributions in April – this will come into effect on 6th November 2022. Good news for you personally, and if you’re a business owner paying team members. Bad news if you’re John, who has now wasted his time updating our tax calculator spreadsheet to take account of increased NICs in July ….

Dividend Tax

The additional 1.25% added on to Dividend Tax in April 2022 will now be scrapped in April 2023. So Dividend tax rates will return to 7.5% for basic rate tax payers and 32.5% for higher rate tax payers. That’s good news for business owners!

Stamp Duty Land Tax

The minimum threshold for paying Stamp Duty on property purchases has been increased from £125k to £250k. For first time buyers, this has been increased from £300k to £425k. This is effective immediately.

It’s a nice nod to anyone in the property market (buy to let investors or those buying second properties will still have the SDLT surcharge however), but I’m not convinced it will soften the blow enough considering the interest rate rises by the Bank of England over the last few months. If you’re in a fixed deal, enjoy it while it lasts. If it’s coming to an end, prepare for your monthly mortgage repayments to increase.

Corporation Tax

The planned increases have been scrapped, so this will remain at 19% for the foreseeable future. No more sliding scale from 20-25% to try to get your head around.

They are also going to simplify IR35 rules for people who operate as contractors/self-employed under a personal company. Full details on this will unravel in the next few weeks ahead of the changes in April 2023.

Energy Prices

Caps are in place in England and Wales to keep annual average bills at £2,500, with every household receiving £400.

Meanwhile, here in Northern Ireland, watch this space. Our energy market is different, so there’s nothing confirmed with us yet (as far as I know). Our domestic bills aren’t nearly as high (yet) so we’ll have to wait and see. I’d imagine the lack of a functioning executive at Stormont won’t help our cause.

Gift Aid – although the basic rate falls to 19% from next year, there will be a four year transitional period for Gift Aid, maintaining income tax basic rate relief at 20% until April 2027

More good news – The planned increase in alcohol duty has been cancelled.

How will all of this affect you?

You might notice a few extra pounds in your pocket when the NIC increase is removed in November. Apart from that, there’s not much to it.

We are all waiting to see how winter goes (have you noticed the price of a bag of coal!!!)

The bigger effect will be on your investments.

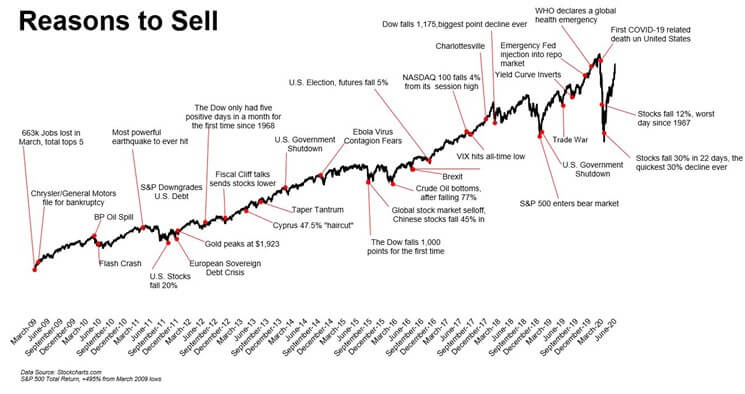

Initial reaction in the investment and currency markets was shock, surprise, concern…. The FTSE closed down 1.97% on Friday. Nothing new here as the daily market volatility we have been experiencing this year continues. Just another day of an almost 2% swing across global markets.

Markets were down around 20% year to date from January to June. Then they pretty much made back most of the ground over the summer. And then, in September, we’re almost back to where we were in June.

It’s not nice if you need the money out of your investments, but our clients are invested for the long term and so this shouldn’t be much of an issue.

It’s great news if you are investing, because you are getting more units of investment funds now for your money than you were at the beginning of the year. For all our clients who are investing monthly, whether that’s through your ISA or Pensions, it’s good news for you.

So what’s the outlook?

Who knows. We don’t guess what happens in the markets in the short term.

Remember, nobody knows if markets are going to continue to decline and if so, for how long. The key is to remain invested, don’t panic, and stay the course.

In the long run, this will be another blip in your very long investment journey.

So, do you need to go and adjust your budget as a direct result of this mini budget? I’m not so sure…

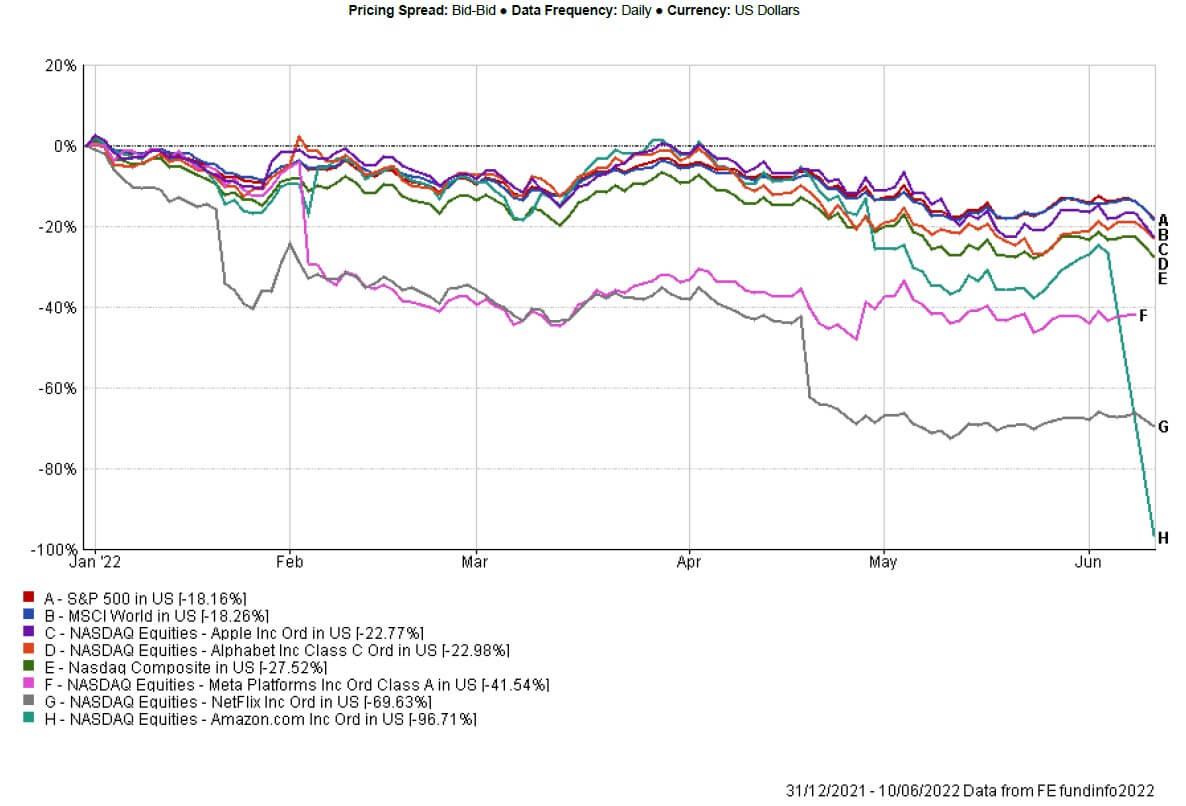

It’s not pretty! *The S&P 500 and MSCI World are both down 18%. The Nasdaq Composite, labelled E above, is down 27.52% until 13th June 2021. At time of writing, the US market is still open and both are currently down a further 3%. This would mean the S&P officially entered a Bear Market today.

It’s not pretty! *The S&P 500 and MSCI World are both down 18%. The Nasdaq Composite, labelled E above, is down 27.52% until 13th June 2021. At time of writing, the US market is still open and both are currently down a further 3%. This would mean the S&P officially entered a Bear Market today.

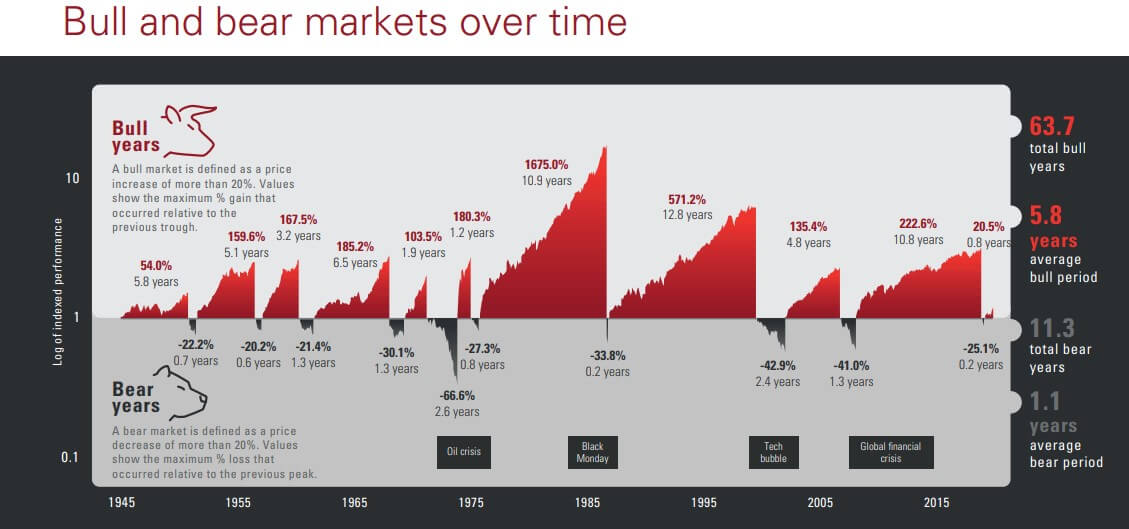

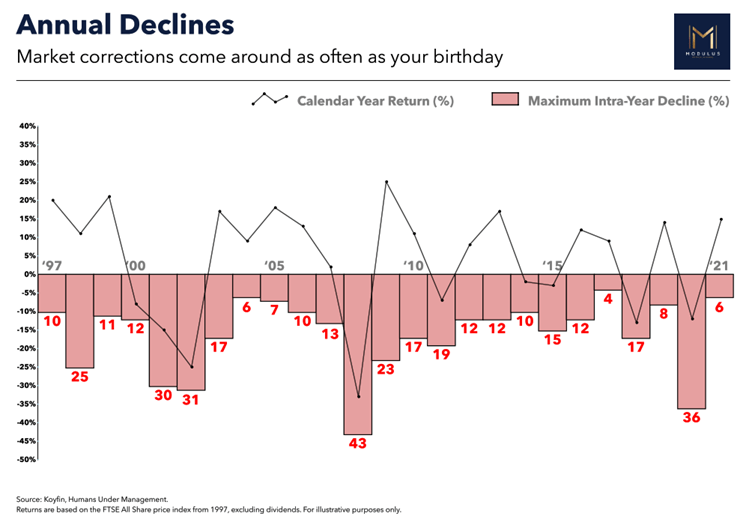

Look at 2020, the second last bar. The biggest decline between February and March (when Covid shut down the world) was 36% for the FTSE All Share.

Look at 2020, the second last bar. The biggest decline between February and March (when Covid shut down the world) was 36% for the FTSE All Share. This shows the importance of investing for a long time.

This shows the importance of investing for a long time.