Recently, I attended the Nextgen Planners Goodstock Ethical Investing Conference in Edinburgh.

Now don’t get me wrong, I am not a full blown “eco-warrior.” I have no ambition to buy a farm and live off grid in a self-sufficient manner. And I don’t have any intention of joining the Just Stop Oil protests. We heard from people who have done these things, but I won’t be following suit.

But what is obvious is the effect on the world that people are having. With climate change and extreme global weather events becoming more evident every year, it’s never been more important to think about what we can do to minimise our impact on our environment. And rather than sit and protest on roads or throw paint on planes or soup on Van Gogh’s Sunflowers, some thing we can do (with no legal recourse) is to think about how we invest our money.

There is a line between the right thing to do and legal laws. In my eyes, the activists cross this line.

We Have A Problem

What was evident is that we have a problem.

Firstly we have a language problem. There are so many labels and names and acronyms that it puts people off. Whether it’s green, deep green, green-washing, ESG, sustainable, Impact, responsible… The investment industry has come up with so many terms and words that it’s become a bit of a mess. No wonder it’s complicated.

We also have a climate problem. There were some very interesting stats thrown out which I can’t back up with evidence here, so take them as you see them.

- Apparently the top soil we have today around the entire world won’t be fertile enough to grow anything in 30 – 60 years depending on how we treat it. Now if we do look after it, it can regenerate. Our modern day mono-culture practices of farming where each field has only one crop doesn’t help. If we allow fields to grow many different plants (re-generative farming if you have watched the latest series of Clarkson’s Farm) can help the problem resolve itself. Or in China, they are trying to reforest parts of the Gobi Desert in their Great Green Wall movement.

- Experts predict we use up so much resources that oil and natural gas will be non-existent in around 50 years. We are working on renewable energy and even today we see solar panels and wind turbines everywhere now, but we need to go further. Elon Musk is probably the most famous here for trying to bring in Solar Roof Tiles.

- Due to our urbanisation and destruction of certain environments, we are increasing the speed of animal extinction. The top 10 animals in danger of extinction include the Polar Bear, the Asian Elephant, the Giraffe, the Tiger and Cheetah and the Red Tuna. If this happens, our children are going to be missing out on many of the key animals they learn about.

- Something which maybe won’t surprise you, is Europe is leading the way on this. Probably not surprising since the US seems to play the “Hokey Cokey” continually stepping in and out of their environmental and sustainability promises depending on who’s sitting in the White House.

With all of these stats, the timeframes are all relatively soon. Just 30 – 60 years.

The scary thought is I’ll still be working in 30 years as will some of our clients. In 60 years, I would be in my mid 90s, so hopefully I’ll be finished with work by then. But this is definitely an us problem, and not a problem for the next generations.

Each presenter had various stats that people are looking for this kind of thing now. As recently as last year, there was a survey they reported that almost 60% of investors would choose to invest in some sort of ethical fund if they had the option.

What are we doing about it?

Without wanting to impose our own beliefs on anyone, one of the things investors can do is to use the influence of shareholder voting rights. Through investing, we own shares in businesses and therefore have a vote at each company’s Shareholder AGM. When these funds which have millions, if not billions, of all of our money, they need to use that vote to hold corporates and companies to account, to develop their sustainable practices to try to help this issue. Two of the biggest fund managers who have been criticised for not doing this as recently as a few weeks ago are Vanguard and Blackrock

Lots of us have money invested, whether it’s savings or our workplace pension. If this money can be used for good, as well as to grow for our own futures, then why shouldn’t we?

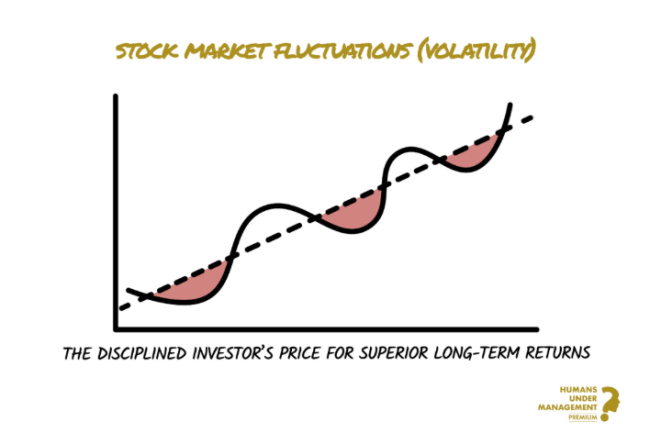

There are lots of things we could do, but one such practice is investing in ESG Portfolios. You can go further if you wish, but the further down the line you go, you reduce the diversification of your portfolio and therefore increase the volatility, which can cost you returns. This is where Sustainable and Impact investing come in. See my video from a few years ago about the Spectrum of Ethical Investing.

We believe ESG (Environmental, Social, and Governance) investing is a good way to align our portfolio with our values without impacting returns. There has been lots made of this recently, as the ESG overlays meant not being as heavily concentrated on the Magnificent 7 when they took off towards the end of last year. Consequently, ESG portfolios also didn’t fall by as much in the last few months when these companies also fell back. The trade off of AI is the energy the computer systems and data houses required to power it.

When anyone looks at investment strategies, they will find evidence for almost anything they want if they take a short term outlook.

What is ESG Investing?

ESG investing considers Environmental, Social, and Governance factors when making investment decisions. It’s about more than just profits—it’s about making a positive impact. Let me break down each part for you:

Environmental (E)

This focuses on how a company impacts the planet. Think about energy use, waste management, pollution control, and protecting natural resources.

Social (S)

The social aspect looks at how companies manage relations with employees, suppliers, customers, and communities. It includes labour standards, health and safety, human rights, and community involvement.

Governance (G)

Governance involves a company’s leadership, executive pay, audits, internal controls, and shareholder rights. Good governance means transparency and accountability. Unilever shines here, with executive compensation tied to sustainability goals and clear, honest reporting.

ESG for the long term

Given the growing threat of climate change, incorporating ESG factors into our investment strategies isn’t just the right thing to do—it’s should be smart finance. Companies that address climate risks tend to be more sustainable in the long run. And if we’re investing for the long run, if all of these companies have deadlines and targets to meet in 2030 and 2050, then this should help long term portfolio returns.

Big funds are leading the way on this. Take the Norwegian Government Pension Fund, also known as the Norwegian Sovereign Fund. As of August 2024, this fund is worth over $1.7 trillion and has shifted heavily toward sustainable investments. They’ve poured billions into renewable energy and moved away from companies that fail to meet their ESG criteria. In 2022, they allocated a whopping $11 billion to green bonds and renewable energy projects, showing their commitment to a sustainable future.

Wrapping It Up

Incorporating ESG considerations into your investment strategy isn’t just about feeling good—it’s about making wise financial decisions that should impact our long term future both financially and as Planet Earth.

One of our key values at Modulus FP has been to choose positive change if we can. To leave the world the way we found it without affecting your day to day life.

There will always be trade offs. We believe if we can help in this way, then we don’t need to feel guilty about taking planes around the world or driving SUVs. We’re not thinking of getting a Glastonbury-esque compost toilet installed nor are we asking you to.

ESG investing is an answer to doing what we can, which takes minimal effort and doesn’t affect our daily routine.

If you want to go one step further then great, but that’s your decision and not for us to impose upon you.