Modulus Financial Planning’s “Technical Tuesday” series covered in National Financial Planning magazine – New Model Adviser.

Click the link to see the article – NMA Technical Tuesday Coverage

Click the link to see the article – NMA Technical Tuesday Coverage

This is the most common question we get asked. Whether it’s a conversation at a wedding, during a meeting, or talking to mates in the pub. “How much do I need? How much should I have? I have £100,000 – is that enough?”

It doesn’t matter how it’s worded, everyone is looking one of two things – either to have something to aim for or to compare themselves against others. It’s human nature to want both of these things, so don’t feel bad admitting it. It seems like a simple question, but the answer is far from it.

We will always answer with a variation of “It depends….” But what we are really asking is “what do you want your retirement lifestyle to look like?”

As you can see the answer is always going to be different for everyone.

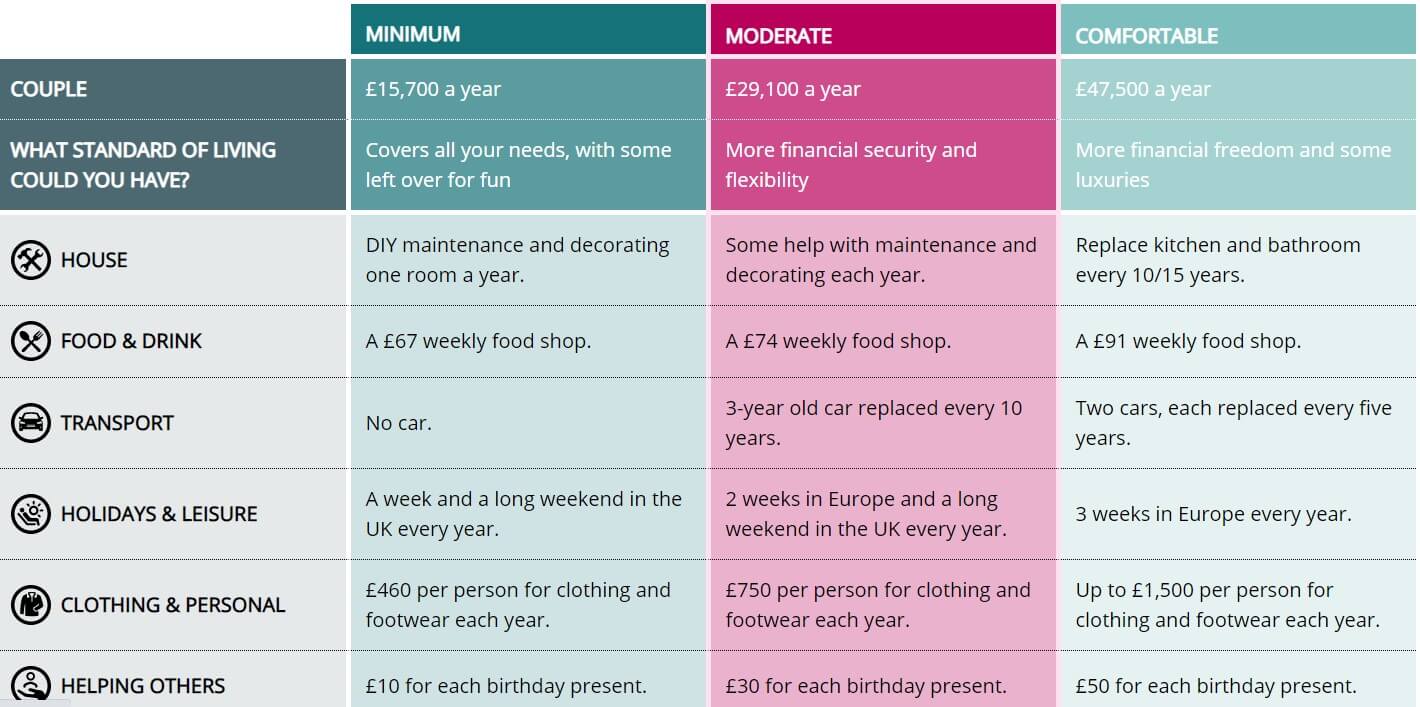

Luckily for us, the UK government did some research to put some figures towards this. Let me introduce you to the Pensions and Lifetime Savings Association (PLSA) Retirement Living Standards study. This study was completed in October 2019 so figures will be higher now (due to inflation) and is a UK average.

The study’s aim was to show how much of an annual income you may need each year. It depends on whether you are single or in a couple, and whether you want a Minimum, Moderate or Comfortable lifestyle.

| Single Person | A Couple | |

| Minimum Lifestyle | £10,200 per year | £15,700 per year |

| Moderate Lifestyle | £20,200 per year | £29,100 per year |

| Luxury Lifestyle | £33,000 per year | £47,500 per year |

To put some context to what each of these lifestyles looks like, they have produced this infographic. This is for a couple:

If you are interested in finding out more, go to https://www.retirementlivingstandards.org.uk/ for full details of their research.

You can only start planning when you have an idea of what your lifestyle will look like, or rather, what you want it to look like. Remember a full current state pension pays £179.60 per week (in tax year 2021-22), which for 52 weeks gives an annual income of £9,339.20. So, a full state pension does not provide sufficient income for a single person to live the minimum standard of living, according to the above research. However, for a couple, with two full state pensions, they would have a combined income of £18,678.40 which does cover the minimum lifestyle for a couple.

Have you other savings or investments which will help to contribute towards this?

There is so much which can come from the question of “How much do I need?”

The thing about the State Pension is that you have no control over when you will receive the benefits (currently age 66, 67 or 68)! So if you want to retire aged 55 then you will need other forms of income to help you live your desired lifestyle.

As a very simple rule of thumb, your pension fund value should safely provide you with an income of 4% per annum. So if you have £100,000 in your pension, you should be able to withdraw £4,000 per annum (increasing with inflation each year) and not run out for 30 years.

You might already know what your income will be in retirement. Or, you have lots of “stuff” and no idea how it all comes together. That’s when you need to start doing something about it.

Here are 3 action points to help you begin your retirement review –

By using the very simple rule of thumb that your income is 4% of the fund, £500,000 would then provide an annual income of £20,000 per annum. To put that in context, for a single person, that provides a moderate lifestyle. However, if it’s split between a couple, you are £10,000 per annum short of a moderate lifestyle.

Would you be happy to settle for a retirement with no car, holidays within the UK and spending just £67 per week on food and drink? If not, now is the time to do something about it.

I am sure that most of you will now have heard that the Government is set to try and fix the Social Care System (in England) by implementing Social Care Reform. The sentiment has been well received, and rightly so, however the Government intends to fund this by increasing National Insurance Contributions (which has received some criticism as it goes back on a general election commitment as well as the impact on younger and lower earning workers).

The plan is to increase National Insurance Contributions (NICs) by 1.25% to 13.5% (for employees – on all sums between £184.01 and £967 / week). That is an increase of over 10% on your National Insurance contributions! An announcement of an explicit increase of 1.25% sounds a bit more palatable than a 10% jump in National Insurance! It’s about how you spin it sometimes, isn’t it?

Not only are employees being hit with this hike in National Insurance, so too are employers. Contributions for employers will jump from 13.8% to 15.05% (on all sums between £170.01 and £967 / week). Again, that is a jump of over 9% on the National Insurance contributions that employers must make for their employees.

Please note that this does not affect people over the state pension age nor anyone taking personal pension income (as no National Insurance is collected on these payments).

The plan is set to raise between £10 – £11 Billion per year. This additional payment, known as the Health and Social Care Levy (HSCL) element, will be separated out and visible on payslips so people will know exactly how much they pay towards this element of National Insurance. This reporting will begin in the 2023 / 24 tax year.

Please note that the Government plans for Social Care reform will not affect Social Care in Northern Ireland, Wales or Scotland as they have devolved Governments and therefore have their own care funding systems. However, as NICs are not a devolved tax, residents in these countries will have to pay the HSCL. The additional payments will however be returned to the devolved nations via the usual allocation formulae.

Company shareholders and those who receive dividend income from their investments are also set for a tax hike. This will look like –

| Tax Year | Basic Rate | Higher Rate | Additional Rate |

| 2021 / 22 (currently) | 7.5% | 32.5% | 38.1% |

| 2022 / 23 (onwards) | 8.75% | 33.75% | 39.35% |

Given the Budget announcement in March regarding the increase in various rates of Corporation Tax from April 2023 onwards, this will mean that company owners should take some time to consider how they take remuneration in the future.

Initially after the announcement in March – dividends looked less attractive. After the announcement last week about a hike in both Dividend Tax and National Insurance – the dividend option looks slightly better (in most cases). The question now is what is best for each individual case? Should income be taken primarily as Dividend, mostly Bonus or possibly a good mix of both? This is definitely one for discussion with both your financial planner and accountant.

There is one – I promise! But only if you are an employee who sacrifices salary into a pension!

Salary Sacrifice is where you give up some of your top line income in order to get some more money into your pension. By sacrificing some of your income you pay less Income Tax and National Insurance. Your employer also pays less National Insurance as well. Quite often employers are happy to pay their National Insurance saving into your pension as the overall net cost is the same for them.

If you are sacrificing some of your salary into a company pension via your employer, and they are contributing their employer National Insurance saving (13.8%) then you are going to get some more money paid into your pension – an additional 1.25%.

State Pensions also took a bit of a hit when the DWP (Department for Work & Pensions) announced that the earnings element of the Triple Lock just won’t apply for the 2022 / 23 tax year. Instead, the basic and new State Pensions will rise by the greater of 2.5% and CPI Inflation to September 2021 (likely to be around 3% based on Bank Of England projections).

The reason that the DWP removed the Triple Lock for next year is because the estimated growth in earnings would be “between 8% and 8.5%”. By taking the earnings element out of the State Pension increase lock for this year it means that there will be a huge saving for the Government. It also means that the base for future increases is set lower, meaning that revenue is saved for the Government moving forward. Look at that – 2 spending cuts in real terms at the same time – a blatant one and a stealthy one!

For the first time in 3 years there will be an Autumn Budget. The date for this is 27th October. It will be a big day for the current Chancellor – Mr Rishi Sunak as he will be presenting the Budget, The Office for Budget Responsibility (OBR) latest Economic and Fiscal Outlook and the 2022 – 24 Spending Review.

So all in all, it turns out hiking is good for your health after all – both physically, and when it’s a tax hike for the NHS budget.

Quite a statement to start off.

The definition of selfish is –

”Caring only about yourself rather than about other people”1

“concerned excessively or exclusively with oneself : seeking or concentrating on one’s own advantage, pleasure, or well-being without regard for others”2

So being selfish primarily means taking purposeful steps to get to where you want to be. It means having the self-awareness to recognise what you want to happen in your life and taking action to get there. Everyone has their own goals and aspirations. Things they want to do and achieve. Not everyone takes the time to really plan to get there. The good thing about taking proactive steps is that it is not only you who will ultimately win. Being selfish with your financial planning will ultimately help empower you to make decisions about your life (not just finances) that can help not only you, but those around you.

Imagine having the context and peace of mind to know that you can do and achieve the things you want personally within your lifetime.

Imagine being able to say to your family “here is some money there to help with your mortgage”.

Imagine the joy of being able to see them enjoy this before you die, when ultimately, they will inherit it.

The thing is that this is a lot of joy that could be shared because you were selfish. You were selfish enough to take the time to figure out what you wanted in life, develop a plan and work towards that.

And it also doesn’t have to revolve around family – it is about what you want. It could be giving a legacy to a charity whilst you are alive – be that through giving money or indeed giving your time.

Imagine knowing that through your selfish attitude towards planning that you could leave paid employment or retire and devote time to a local charity or voluntary organisation.

Imagine the freedom and the feeling you would have and the impact that your selfishness could have on helping others.

Imagine spending more time with your family or looking after grandchildren (on your terms). The selfishness that you showed about planning your life could have a much wider impact on so many other people. Imagine the feeling your financial planner has when she / he helps you to do all this. It is a feeling that is hard to describe. To be able to help someone do what they want, when they want to is incredibly empowering. It also helps that I get paid to work in such a great role.

I believe that Financial Planning is selfish and that it should be. It should always be about making sure that our clients live the lives they want to. It is a selfish pursuit but one that has the potential to bring happiness and enrich the lives of so many people – and it isn’t all about the money – imagine that!

This material is aimed at retail clients and is for information only and should not be considered as a personal recommendation.

1 – https://www.oxfordlearnersdictionaries.com/definition/english/selfish

2 – https://www.merriam-webster.com/dictionary/selfish

Something very important to us here at Modulus FP is that our clients are living the life they want. Not only are they living the life they want now, but also making sure to be putting away for their future. The only way you can do both is by making sure to find the balance between spending for now and saving for your future.

One of the first, most important rules we should all be living by is to spend less than you earn. For obvious reasons, if you are continually spending more than you earn, it’s not going to end well. Popularity of Buy now Pay later schemes is rising. We can use them for a new TV, clothes from almost any online shopping site via something like Klarna, or even for laser eye surgery. We must be careful to make sure we only spend what we can afford.

According to The Money Charity Money Statistics in May 2021, people in the UK owed £1,712.9 Billion at the end of March 2021. Broken down, this is an average household debt of £61,435 which per person, is around 110.3% of average earnings. Now, this isn’t surprising when you consider that the bulk of this money is mortgage lending. But total unsecured debt per adult is £3,712 and the average credit card debt per household in March 2021 is £1,945. After the year we have been through, this has reduced by 21.7% compared to the previous year. So we are making moves in the right direction. As things start to open up, we can go out again and spend money, and hopefully we will be able to travel again too. As a result, most of us are going to start spending again.

If you were one of the lucky ones whose income has been steady and secure in the last year or so, your bank account might have been steadily increasing. Most people used it to pay down debts, and now they have a decision to make. Do they spend or do they save?

“Lifestyle Creep” is the title given to the pattern which develops when we have more money available. This is a result of either an increased income or a decrease in spending. We start spending this money on luxuries, which starts a habit and these become an every day expenditure rather than a luxury. It begins with little things like a takeaway coffee every Monday to start the week. Or doing your grocery shopping in M&S instead of Tesco. Or you might decide you need a more luxurious brand of car. Or you might think your blue and white striped shirt needs to have a logo on it, so start spending £50+ on a shirt.

It’s something that is easy to fall in to, but very difficult to get out of. So how do we stop it?

You should try to decide on the balance between spending money for now and saving money for the future. Once you have decided that number, set up a standing order for the day after you get paid, to send the money out of your account. Preferably, this money is going into an investment. This way, you are always buying into the market whether it is “high” or “low.” This is a great habit to get in to. Once you don’t notice the money going out of your account, that’s the time to reassess the amount and increase it. We like to call it “Giving Yourself a Pay Rise.” When was the last time you gave yourself a pay rise?

The key to this is finding the right balance. The balance between spending and enjoying your life now, but also making sure to put away for your future. We’ll never suggest to save all of it, because then you run the risk of not living today. Likewise, we’ll probably not tell you to spend it all, because then you aren’t giving yourself as many future options.

When you get a pay rise or your monthly payments on your car finance ends, reassess your position and consider saving some of the money. Otherwise, you’ll likely spend it, and the cost of your lifestyle will creep upwards.

This is aimed at retail clients and is for information only and should not be considered as a personal recommendation.

Investments can go down as well as up, and you may not get back the full amount you originally invested

And the other one “sure ISAs are terrible at the moment!”

These are a couple of things we often hear from people. We may hear it when we are first meeting a prospective new client. Or when we are talking to someone on the street (and they find out what we do for a living). We also see it on social media channels like Facebook when the Keyboard Advisor is giving everyone their take on pensions (and usually why they are terrible!).

Things like a pension or an ISA are wrappers. They are ways of holding money with their own tax advantages and disadvantages. I have created a short video to help explain this (click here to view as well).

I hope the video helps to explain what exactly a tax wrapper is and that they aren’t useless or terrible.

Some of the things that tax wrappers can do include –

Tax wrappers are very useful when thinking about your long-term financial planning.

As in the video – what you get out of the mug / tax wrapper can depend on many things but mainly by what you put in.

If you hold cash in an ISA and expect to beat inflation over the long term, then you may well be disappointed.

You are unlikely to have a positive investment experience if your pension –

There is a much greater chance of having a successful and positive investor experience if your portfolio

If you haven’t considered what you hold in your various investment wrappers, then now is a good time to drop us a line. Reviewing what you hold to ensure it aligns with your financial plan is important. It gives you context in relation to your long-term financial security.

As always, we want to hear your thoughts and appreciate your feedback. If you want to contact us then you can do so on hello@modulusfp.com, on the phone or through our social media channels.

PS – please note that other types of tea are available apart from Earl Grey. It just so happens that this is the only tea I am aware of (apart from the normal breakfast kind) so apologies!

Please note – the money you invest is at risk and could go down as well as up and you may not get back what you have invested.

‘Avoid the bus question’: IFAs on dealing with death in 2021

Discussing-death-with-clients.pdf (411 downloads )

Now that it’s April, we are now into a new tax year. It’s not as popular as the 1st January new year, or the Chinese new year, but this is arguably the one which affects everyone the most. Some things have changed, but lots haven’t – so here’s the lowdown.

*(Quick question first – from what film was the title taken from? Answer at the end )

The good news is that your personal allowance increased this year with inflation – by just over a massive 0.5%. This is the amount of money you are allowed to earn in the year on which you don’t pay any income tax. This increased from £12,500 to £12,570 (or £1,048 per month). Don’t spend that extra tax free £70 all at once! In reality, this will only benefit you by the tax no longer due on that £70 which would be a massive £14! Seriously – don’t spend it all at once.

You’ll pay basic rate tax at 20% on everything you earn between £12,570 and £50,270, and then higher rate tax at 40% on income between £50,270 – £150,000, and additional rate tax over and above that at 45% .

It’s not all good news though, because they have frozen these thresholds for the next 5 years until 2026, so if you’re lucky enough to be in a job which has guaranteed pay rises, you will actually pay more tax.

Call me ungrateful, but for my own brain, I kind of wish they could have stuck with the nice round numbers of £12,500 and £50,000.

Keeping these thresholds and allowances the same for a while is a way to increase the amount of tax being paid over time. Wages will rise but as the thresholds and allowances are staying the same, it means that more tax will be paid. This is what is known as a stealth tax – you may have heard about it on the news. More stealth tax news to follow!

For those families with children who are claiming child benefit, something which might affect them is the high income child benefit tax charge. It kicks in after you (or your partner) start earning over £50k. For every £100 you earn over £50,000, you have to pay back 1% of the child benefit you received. Therefore, if you earn over £60k, you have to pay it all back.

The unfair part, in my eyes, is that this applies if only one parent earns over £50k. So, if a husband and wife are claiming benefit and both earn £50k – which is a combined household income of £100k gross – they are fully entitled to child benefit. However, if one earns £60k, and the other doesn’t earn anything – so they have a combined household gross income of £60k – there is no entitlement to child benefit.

This isn’t new, but what is new, is that this could actually affect basic rate taxpayers for the first time! There doesn’t seem to have been any update on the £50k threshold for this, and so with new Tax Bands, you may be a basic rate tax payer and still need to repay child benefit should you earn between £50,100 and £50,270. Did someone say Stealth Tax?

No changes here.

For another year, they have frozen the ISA allowance at £20,000. This is the amount an individual can pay into their Individual Savings Account(s) in total in the tax year. It has been set at £20k since April 2017. This is a “use it or lose it” allowance, and so make sure to use as much of it as you can. As ISAs grow free of tax, whether in cash or invested, this is a valuable benefit and so if you can, try to use your ISA allowance as early as possible to start earning tax free.

Junior ISAs – saving for your children – have an allowance of £9,000, which is the same as last year as well.

Lifetime ISAs – saving for your first home or until age 60 – has stayed the same with an allowance of £4,000 which the government will add a further £1,000 on to.

These ISA allowances are also frozen until 2026.

Again, not much excitement here. Your annual allowance (how much you can contribute in this tax year without taking advantage of carry forwards) remains at a maximum £40,000. However, unlike an ISA, you can carry forward any unused allowances for the last 3 years. This means that provided you have been a member of a pension scheme, the maximum pension contribution you could potentially make in this tax year is £160,000. Please note that in order to gain tax relief on personal contributions you will need to have taxable earnings up to the amount you are contributing to the pension e.g. to contribute £100k using Carry Forward you will need to have earned income of £100k. For information about employer contributions download our “Coffee guide to pensions”.

Lifetime Allowance however has been frozen at £1,073,100. This is the total amount you can have saved in a pension. This is where some people may come unstuck, as with investment return in your personal pension (defined contribution pension), or revaluation if you are lucky enough to be in a final salary (defined benefit pension), you may increase above this allowance if you were close to it last year. The Lifetime Allowance for pensions is also frozen until 2026! Again, another example of stealth taxation in practice!

The full State Pension went up by 2.5% to a weekly pension of £179.60 (up from £175.20 per week) Two full state pensions could now pay a retired couple over £18,500 per annum, guaranteed. Bear in mind, because of the triple lock, pensioners got a 5 times inflation pay rise this year!

No change here. The government have frozen your capital gains allowance at £12,300 for another year. If you’re a basic rate tax payer, you’ll pay 10% or if you’re a higher rate tax payer you’ll pay 20%. If the gain is on property (not your main home) then there is an additional 8% surcharge). Again the Capital Gains Allowance is also frozen until 2026, meaning an effective tax increase in real terms. I’m actually going to stop pointing out these examples of stealth taxes now!

No change here. Another year of frozen Nil Rate Bands (the amount on which you can pass on without paying Inheritance Tax). These rates are also frozen until 2026. Again as the value of your estate increases over time the likely result will be more tax paid. Maybe if I use the word Covert instead of stealth – would that be less repetitive?

All in all, apart from the crafty tax increases (read stealth tax here) there is not much change from last year. I think we were all braced for increases in personal tax given the year we’ve just had, but maybe most of us weren’t expecting them to be so implicit. The big headline changes hit business owners with Corporation Tax changes. They had the explicit tax increase from 19%, stepped up to as much as 25% if earning significant profits.

There are however opportunities available to business owners, especially in terms of retirement planning. We can only work to the rules laid down but it would appear that now is a pretty good time to review your financial planning with a view to making sure that all your ducks are in a row moving forward. Book some time to talk over your financial planning with us

*The answer to the question above was of course Trading Places (1983) starring Eddie Murphy & Dan Aykroyd

Let’s start with why because one of the most important parts of financial planning is the Why?

For each person, the why will be different. Most people will all roughly have the same high level goals such as –

The reasons someone will have their own financial plan will always be very different.

Some clients may want to retire over time. They might do this to help look after their grandchildren. Some will want to be able to trek Machu Picchu when they are young and fit. Some may want to be able to take their extended family on holiday year in, year out. It doesn’t matter what the why is. But it is important to identify it and work towards it. When we work out the why then we can start the process of understanding what financial planning is.

Financial Planning is about helping people to find a balance. That balance is between their income, current expenditure levels and future expenditure needs. Wait, is that it? Well yes that is all financial planning is (kind of). There are many other, in depth ways of explaining the concept of financial planning. There are big words that can help explain how financial planning work. But I intend this to be a somewhat simple read (I hope) that won’t be too confusing and full of jargon.

Everyone should have a financial plan of some description. That doesn’t mean everyone needs a huge in-depth report. Not everyone will need all the detail of their spending replayed over the course of their life. Everyone should consider having a personal roadmap of their financial planning. This is their financial plan. This may be as simple as writing down some goals and how they might start the journey of getting there. There aren’t many people who would consider taking a road trip across say America without having a plan. They will consult a map or use a sat nav to give them directions. Well life is a long journey. If you want to know where your finances will take you then a financial plan would be quite helpful.

This is always an interesting question. You might think that you will only need a financial plan when you’re in a position to invest money. Or if you are of a certain age (some people think you need to be in your 40’s to need a financial plan). But you can start thinking about financial planning at any age. In fact, the sooner the better. Someone in their 20s’ who has started a new job needs to consider their financial planning needs. They need to just as much as someone in their 50’s who is planning for retirement in the next few years. What would happen to our twenty something if they weren’t able to work for an extended period or even ever at all?

We see that there is a real lack of financial understanding in society. That is part of our why here at Modulus. People have many questions about financial planning. They often don’t know who to turn to. They sometimes don’t know who to trust. They need help understanding the workings of the products out there. People need a guide to help cut through all the jargon and sales patter. Some people are afraid to ask a question in case it sound silly and that should never be the case. Over time we would like to build a portal for clients and their families. The aim would be to help increase financial education and understanding. It would have articles and tips to help people with all aspects of financial planning. But for now, please bear with us or feel free to drop us a line with any questions.

Identifying and understanding “Why” is huge when beginning the financial planning journey. Goals need to be set for a successful financial planning journey. If there are no goals, then it is a case of accumulating money for no reason other than to have it. Taking the time to speak with an Independent Financial Planner will help with this.

Some people don’t think they’re ready to speak with a Financial Planner. There are still steps that can people can take to start the journey though. One of the easiest and most effective things to do is to make a list of spending. Record it on a spreadsheet or even write it on a piece of paper. The best way to do this is to look at bank statements. Also look at credit card statements (if used). This makes sure actual figures are being used rather than guess-timates! The results may well prove surprising. And do this for the last 6 months statements at least. This will help to give a longer-term view of spending. It will help to smooth out the effects of the expensive months that everyone has. Remember there are times when spending will be higher e.g. holidays, family birthdays etc.

Once there is a log then creating a budget becomes a much easier task. This is because of there is a better understanding of spending trends and habits. Adding funds to a specific goal at the start of the month will create discipline. Do this after payday. Don’t set out to try to save excess funds at the end of the month. This won’t work because something will always “be found” to spend it on! Pay yourself and your goal pot first. This creates positive action towards reaching the elusive “Why”. Which is of course different for everyone.

The thing to remember is that Financial planning is a way of helping people to live the life they want”.

If you want to start your financial planning journey then feel free to drop us a line to arrange a 15 minute chat. We can do this either online or at our offices over a coffee (at no charge). We’ll even supply the coffee.

And it’s ok if you’re not ready for a chat but want to get started. Take the first step! Download our One Page Annual Budget Planner.

If you’ve any questions then you know where to find us!

“Always plan for the fact that no plan ever goes according to plan” Simon Sinek

This quote, from Simon Sinek, always stuck with me. He is most famous for his book Start With Why and TED talk, but has become a business and leadership influencer.

It might seem strange for a financial planner to admit that a plan never goes according to plan, but it’s true. It’s the act of planning and reviewing it, rather than the plan itself which is the important part. It’s also why we’ll add in alternative scenarios where things might not go to plan.

As most will know, I’ve had an eventful year or so. When I made the decision to leave my previous job, I made a plan on how I was going to get by. I had a 6 month non compete in the whole of financial services. That meant I wasn’t going to be working in what I do for 6 months, and so I wasn’t going to be earning. I needed to live off my savings. So I started saving for when the time came for me to pull the pin.

One thing led to another, and I ended up making a very quick decision to quit. I knew I had enough to scrape by, and thought I’d get a job doing something in the meantime. I quit and then had the most eventful day ever. I handed back my work laptop at 2pm on a Thursday, and then my youngest daughter, Katie, was born at 5.05pm on the very same day. All a sudden, I had no income and an extra mouth to feed.

What more motivation do you need?

But I had planned for it. Yes, I walked away earlier than I thought, but I thought I could manage. As time went on, you start to notice that things still affect you emotionally more than you thought.

There’s an area of finance called behavioural finance. It’s all about making decisions with your head, and sticking to them. Drown out the noise of all the news, the emotions when things happen and you should be OK if the plan was half decent.

I’d never properly experienced it or been aware of it. It was only by quitting, that I opened my eyes. I’ve always made plans and stuck to them. It was only when I started seeing my savings fall that I became aware of it. How your heart can rule your head when it comes to money.

The real point when I started to rethink if I made the right decision was when my savings came down below £10k. That’s when I started second guessing and starting thinking. Had I done the right thing?

I’ll never know what would have been. But sitting now, knowing that I’m doing something I enjoy with a renewed sense of purpose – I’m sure it is the right thing. But this got me thinking, all I was talking about was reducing £20k savings to £10k and starting to panic. That’s nothing compared to what our clients go through.

Imagine what it’s like if you retire? You go from earning decent money, to living off your pension. That would be scary. And I’ve never properly appreciated that.

You will be watching your money decline. You’ve focussed on building your savings all your life. That completely reverses. You also have lots of time to fill. My first weeks and months of unemployed life were easily filled with a new born and my eldest daughter. The added benefit of my wife off on maternity leave, so I had plenty to be at, and plenty of company too. But that’s an exceptional circumstance.

Whether you planned for it, or something happened which meant you had to stop work, it isn’t easy. It’s bad if it’s a government imposed lockdown which made you close your doors. It’s worse if it’s an illness or injury which suddenly causes it. Too often we get caught up in the financial side of the planning. You need to pay attention to the emotional and mental consequences of it too.

Working in financial planning doesn’t mean we are only concerned about your money. We help you with planning your life first, and then we will do all we can do to make the finances work to be able to afford it.

Download your Investment Guide Here

Modulus Financial Planning look forward for you to contact us for more information about any of our products or services.

Suite 12, Avonmore House,

15 Church Square, Banbridge,

BT32 4AP, Co.Down, Northern Ireland

Here for all your saving & investment, pension & retirement planning, tax & estate preservation and insurances.

Modulus Financial Planning Ltd is authorised and regulated by the Financial Conduct Authority. We are entered on the FCA Register under reference 965916. Registered in Northern Ireland, Company Number NI673772.

The guidance and/or advice contained within this website are subject to the UK regulatory regime and are therefore targeted at consumers based in the UK.

The Financial Ombudsman Service is available to sort out individual complaints that clients and financial services businesses aren’t able to resolve themselves. To contact the Financial Ombudsman Service, please visit www.financial-ombudsman.org.uk.